Money Runs Out Before the End of the Month for a few repeatable reasons, and none of them require a “bad with money” label. Timing problems hit first, then small daily choices finish the job, then a credit line covers the gap at a brutal price.

Brazil adds extra pressure because household costs move fast, and debt is widely available when cash gets tight. IBGE reported 4.26% inflation in 2025, which quietly raises the floor on groceries, utilities, and transport month after month.

Why Money Runs Out Before The End Of The Month: Brazil

Brazilian cash flow often collapses because bills cluster early, spending spikes right after payday, and tracking stays loose until the balance looks scary. CNC’s household debt surveys have hovered around the high 70% range for families, and that background matters when any surprise shows up.

Banco Central do Brasil credit data also shows a high-cost reality for consumer credit, which turns “temporary” shortfalls into multi-month problems.

A paycheck can look fine on paper, then vanish because the calendar is doing most of the damage. Rent, condomínio, utility bills, commuting, and debt minimums land early, while the rest of the month still needs food, school items, and normal life.

The Three Patterns That Drain A Paycheck Fast

These patterns usually run together, which is why the month feels like it collapses all at once. One mistake rarely causes the whole problem. A tight first week, a few reward purchases, and a couple of “small” transactions can stack into the same outcome. Fixing the pattern works better than chasing one-off cuts.

Front-Loading Bills and Commitments

Front-loading expenses means big obligations get paid in the first days, leaving less cash for the weeks that follow. Rent and utilities matter, so the issue is timing, not responsibility.

A calendar that forces heavy payments into one window makes the rest of the month fragile, especially for anyone paid monthly or on uneven dates.

Payday Euphoria and Impulse Buys

Payday euphoria is the emotional spike that turns “deserved” into “spent” within days. Small upgrades pile up fast: delivery fees, a quick shopping app purchase, a nicer weekend, extra top-ups, and another subscription.

Each one feels manageable, then the month turns into counting coins and waiting for the next deposit.

Mental Buckets That Don’t Match Reality

Mental accounting shows up when money gets treated as separate piles that don’t really exist. “Food money” feels protected, “fun money” feels endless, and the real bank balance gets ignored. Everything still comes from the same account, so overspending in one category creates chaos later, even if the original plan looked balanced.

The Quiet Leak: Spending That Never Gets Logged

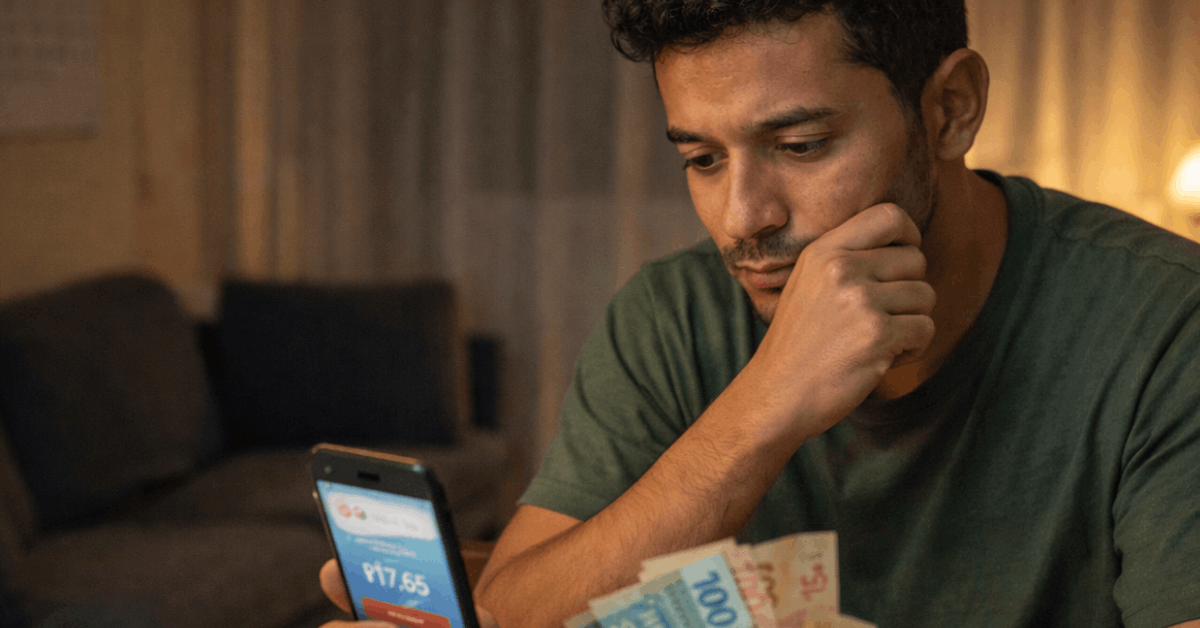

The biggest surprise for many people is how much money disappears without a clear memory. That coffee, that extra ride share, that market run, that “urgent” purchase that was not urgent. A month of tiny decisions can beat one big bill.

track daily spending for thirty days and the pattern usually shows itself within a week. Receipts matter, bank notifications matter, and Pix confirmations matter.

A short note in a phone app works, and a simple spreadsheet works, as long as entries happen on the same day. Consistency beats detail, since the goal is spotting repeat leaks rather than building an accounting system.

Build A Plan That Matches Brazilian Pay Cycles

A budget that ignores timing often fails even when the numbers look correct. Expenses arrive on dates, not in neat monthly averages. A plan built around weeks tends to feel more realistic because it matches grocery cycles, transport top-ups, and weekend spending.

Weekly budget planning also prevents the classic “good first half, disaster second half” pattern. Fixed costs still get paid, then the remaining money gets divided into weekly caps that include food, transport, and personal spending. That cap becomes the decision tool, not the emotion of the moment.

- Map bills and due dates on a single calendar view, including cartão minimums and subscriptions.

- Divide variable spending into four weekly caps, adjusting for five-week months when needed.

- Set a weekly “life happens” line for small surprises, not true emergencies.

- Remove saved card details from shopping apps to slow down impulse purchases.

- Check the plan twice a week, not once a month.

Make Saving Automatic, Not A Mood

Savings fail when they depend on leftover money. Leftovers rarely exist after bills, cravings, and small surprises take their turn. Automation makes saving boring, and boring is usually the point. A small, repeated transfer often beats a big, occasional plan that never happens.

Pay Yourself First Without Waiting For Leftovers

Pay yourself first means saving occurs immediately upon income, not at month-end. Automatic transfers can route money to a separate account the same day the salary arrives. Some banks also support scheduled transfers tied to payroll dates, which helps people paid monthly, biweekly, or on irregular contracts.

Build An Emergency Buffer That Protects The Month

An emergency buffer keeps a surprise from destroying the entire plan. Start with a target that feels reachable, such as one week of core expenses. Add to it every payday, even if the amount is small.

That buffer reduces the need to rely on expensive credit when a tire blows, a medical cost appears, or a family request hits at the wrong time.

Stop Debt From Filling The Gap

Debt often feels like a solution because it buys time, then it becomes the reason time keeps getting purchased. Credit card revolving interest in Brazil has been extremely high, and Agência Brasil reported rates above 450% per year in 2025 based on Banco Central figures. That kind of cost turns a short gap into a long chase.

Cheque especial is another common trap because it activates quietly and charges heavily. Bank apps make it easy to miss the moment it starts, especially when automatic debits hit. Alerts help, but structure helps more: bills in one account, spending in another, savings in a third. Separate accounts create real friction, and friction prevents accidental overdraft use.

Debt control also includes renegotiation when payments no longer fit. Serasa’s Limpa Nome campaigns and bank renegotiation programs can lower interest or extend terms, depending on the case. A renegotiation still needs a new spending plan, or the next month repeats the same cycle.

A Simple 30-Day Reset

This reset works best when treated as a short experiment, not a personality change. The goal is stable cash flow, fewer surprises, and a month that ends without panic. A clean month also reveals how much income is truly available for goals.

- Log every transaction for 30 days, including Pix transfers, delivery fees, and small top-ups.

- Lock a weekly cap for variable spending and track it twice a week.

- Automate savings on payday, even if the amount feels “too small.”

- Build one week of emergency buffer before chasing bigger goals.

- Reduce high-cost credit exposure by avoiding revolving balances and overdraft use.

Last Thoughts

Money Runs Out Before the End of the Month more often because of timing and behavior than because of salary size.

Structure changes the outcome without turning life into a punishment. Tracking, weekly caps, and automated saving create room to breathe, and that room protects decisions.

Brazil’s cost of credit makes “temporary borrowing” far more expensive than it looks on the screen. A calmer month usually starts with routine, consistent steps; the results then show up without drama.